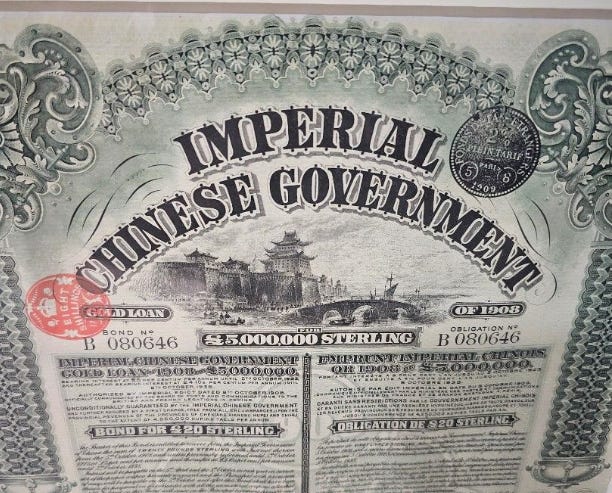

China’s Defaulted Gold Bonds

Are China’s pre-1949 gold bonds still enforceable?

At first glance, the question appears legal. China issued foreign bonds before 1949. Many were defaulted on. Some were linked to gold and carried interest. Holders, or their successors, still exist. So are the bonds still enforceable?

The narrow answer is that enforceability appears doubtful. The broader answer is more interesting. The legal obstacles are substantial, but the issue does not disappear simply because the courtroom path is narrow. In a world of rising gold prices, renewed monetary stress, and sharper geopolitical division, old sovereign obligations can regain strategic relevance even when private recovery remains difficult. That is why the question matters.

The starting point is legal rather than rhetorical. These bonds were issued by earlier Chinese governments before the establishment of the People’s Republic in 1949. Bondholders have long argued that a change of regime does not automatically erase sovereign obligations. That argument is not absurd. States often inherit debts across changes of government, and continuity of obligation is a familiar principle in international finance. A sovereign cannot normally escape every past obligation simply by changing political form. If that were true, the continuity of state finance would become impossible.

But that principle does not solve the enforcement problem. The route from historical obligation to present recovery is obstructed by several layers of difficulty. One is sovereign immunity. Another is the extreme age of the claims. Another is the question of limitations. Another is the practical reality that courts are often reluctant to transform long-dormant disputes of this kind into present-day collection mechanisms against a foreign state. The issue, in other words, is not whether bondholders can tell a coherent story. It is whether that story can still be made legally operative.

That distinction matters. A claim can be serious in historical and moral terms yet still be very difficult to enforce in practice. It is one thing to say that a sovereign debt once existed, that it was defaulted on, and that the legal personality of the state did not disappear. It is another to say that present-day courts will supply a clean remedy, free from immunity barriers, procedural defenses, and the institutional caution that typically surrounds disputes involving foreign sovereigns. The key legal point is not that the historical obligation is incoherent. It is that modern enforcement runs into a wall of sovereign immunity, extreme delay, limitations problems, and judicial reluctance to reopen century-old sovereign debt disputes. Those barriers do not prove the bonds are morally or historically meaningless. They do make straightforward recovery highly uncertain.

This is where the essay must remain careful. It would be too strong to say that the bonds are clearly enforceable. It would also be too strong to say that they are legally meaningless. The more disciplined conclusion is that the enforceability case appears weak in any simple private-law sense, but weak enforceability is not the same thing as irrelevance. A claim can be difficult to win and still become strategically inconvenient.

One reason is that sovereign immunity changes the character of the dispute. Immunity does not necessarily answer the moral or historical question. It often prevents that question from being converted into an effective remedy. This is one reason Sovereign Immunity — A Remarkable Injustice is a useful companion essay. That piece explains how sovereign immunity often operates less as a neutral procedural doctrine than as a form of institutional insulation. The present essay is a practical example of that problem. Even if the underlying story has force, the modern legal structure may still prevent it from becoming easily actionable.

The age of the bonds adds another layer of complexity. The older a claim becomes, the more every surrounding difficulty hardens. Records become harder to standardize, chains of ownership become more complicated, limitation arguments become more powerful, and courts become more cautious. What might once have been a straightforward financial dispute gradually shifts into something closer to legal archaeology. That shift matters because it changes not only the evidentiary problem but the judicial mood. Old claims are often treated not simply as claims, but as disturbances to settled order.

Quantification also matters. The original face values belonged to a very different monetary world, but gold linkage and long periods of accrued interest can produce present-day estimates far larger than casual readers might expect. The precise figure depends on the bond series, the treatment of gold clauses, the interest calculation, and the valuation date. That is one reason the issue remains contested. But the broad point is clear enough: once gold rises sharply, the numbers stop looking merely antique. In one recent U.S. case involving a subset of these historical bonds, the claimed damages were put at more than $11.5 billion, even though the suit was dismissed. That does not establish a recoverable sum. It does show why the issue can become economically legible once gold rises and attention returns.

And yet that is precisely why these bonds remain interesting. Legal enforceability and strategic significance are not the same thing. An old sovereign debt instrument can be too stale, too contested, or too jurisdictionally awkward to produce straightforward collection, yet still remain useful as a pressure point, symbolic grievance, or bargaining chip. In a calm monetary world, that sort of claim remains archival. In a more adversarial world, it can become inconvenient.

In practice, much of this issue may be political rather than purely judicial. A sovereign debt claim does not need to sit on a clear and immediate path to courtroom recovery in order to become dangerous. If relations deteriorate sharply, powerful states can freeze, control, redirect, or otherwise target foreign assets within their reach, especially where those assets sit inside friendly jurisdictions or pass through institutions already subject to political influence. In such moments, the legal, financial, and political arms of the system do not necessarily behave as separate worlds. They can move with a common strategic purpose. That does not mean China’s old gold bonds are about to be enforced through asset seizure. It means that once a historical claim becomes politically useful, substitute assets or vulnerable assets within reach may attract attention even while the underlying litigation remains unresolved. What seems unlikely in one phase of the international system can become much more plausible in another, and the world can change quickly. The broader pattern of freezes, controls, and redirected foreign-state assets in recent years makes that possibility hard to dismiss entirely.

That possibility becomes more sensitive if gold itself is involved. Gold held in, moved through, or custodied within friendly jurisdictions is not simply inert property. In a harsher political environment, it can become part of a larger contest over claims, leverage, and sovereign pressure. The higher gold rises, the more visible the underlying claim becomes. The more polarized the international system becomes, the less safe it is to assume that old obligations will remain quarantined inside technical legal debate. A claim that is weak in private-law terms can still become troublesome if politics begins looking for an available instrument.

This is where gold becomes central. If these were merely obscure paper claims from a vanished era, their significance would be limited. But gold-linked debt is different. Its practical and symbolic meaning changes as gold changes. When gold is quiet, legacy gold clauses look antique. When gold becomes volatile, rises sharply, and reenters public consciousness as a reserve signal, the same instruments begin to look less inert. Obligations that adjust by reference to gold, especially where interest also continued to accrue in theory, become easier to rediscover and harder to dismiss as purely historical curiosities.

That point matters because the issue is not static. The same dormant obligation means something different in different monetary environments. In a world where gold has little monetary relevance, these bonds recede into obscurity. In a world where central banks buy heavily, where reserve distrust rises, and where gold again functions as a visible marker of sovereign caution, the old bonds begin to sit in a different light. They are still difficult to enforce, but they are no longer culturally or strategically invisible. This also connects directly to Gold as Signal. That essay explains why official gold behavior should be read as sovereign positioning rather than ordinary market demand. The present essay extends that logic into a more unusual area: if gold is once again becoming more important in sovereign behavior, then old gold-linked obligations may also become more sensitive.

The East–West dimension sharpens the issue further. In a less polarized world, a legacy bond dispute remains mostly a technical curiosity. In a more polarized one, it can be reframed as narrative leverage. It can be used rhetorically, politically, or diplomatically even where full judicial recovery remains unlikely. A dormant claim does not need to be clearly enforceable to become strategically inconvenient. It only needs to be capable of recurring at moments when broader tensions make it useful.

That is why the question should be framed from China’s point of view as well, not only from the point of view of bondholders. This is not an anti-China argument. It is almost the reverse. A state with long time horizons usually prefers to reduce avoidable legacy exposures before those exposures become useful to others. That is especially true when the issue touches financial credibility, historical continuity, and the changing monetary role of gold. A matter that appears laughably remote in one decade can become more awkward in another if it aligns with a larger shift in reserve politics and bloc competition.

There is also a comparative lesson here. States have often concluded that old debt problems are worth resolving not because the legal case against them is overwhelmingly strong, but because continued ambiguity carries its own cost. The clearest example is Russia’s 1996 agreement with France to settle Tsarist-era bond claims, a dispute that had survived revolution, repudiation, and decades of dormancy before being resolved on controlled terms. The point is not that China must follow the same path or that the situations are identical. It is that long-buried sovereign debt can return as a live policy question, and governments sometimes decide that negotiated closure is preferable to indefinite friction. Old claims are sometimes resolved not because they are easy to enforce, but because leaving them unresolved becomes less attractive than disposing of them on controlled terms.

That comparative point matters for China’s old gold bonds. The real question is not whether bondholders can simply force China’s hand. They probably cannot. The more serious question is whether China may eventually judge that continued repudiation, ambiguity, and piecemeal litigation serve it less well than quiet review, managed retirement, repurchase, or some other controlled architecture that removes the issue from the field. That is a strategic question, not merely a legal one.

It is also a question that becomes sharper as gold rises. If gold-linked clauses imply a larger effective obligation when translated into present terms, then the issue changes character. It remains legally difficult, but economically more visible. Rising gold does not magically create enforceability. It does, however, increase the potential symbolic, political, and narrative weight of the underlying claim. The higher and more volatile gold becomes, the easier it is for such bonds to attract renewed attention. Recent gold-price volatility only reinforces that broader point.

The deeper lesson is that sovereign debt is not always finished when markets stop paying attention to it. Sometimes it passes from finance into history. Sometimes it passes from history into strategy. China’s pre-1949 gold bonds appear to sit in that intermediate zone. Their direct enforceability may be weak. Their complete irrelevance is much harder to assume.

So are China’s pre-1949 gold bonds still enforceable? Probably not in the simple way some holders would hope. Sovereign immunity, delay, limitations, and judicial reluctance all stand in the way. But that does not make the bonds meaningless. It means their significance has changed. They now matter less as a straightforward collection claim than as a dormant strategic issue that could become more inconvenient in a world of higher gold, sharper bloc division, and growing sensitivity to sovereign monetary credibility