The Hidden Monetary System: How the Eurodollar Network Runs Global Finance

Why most of the world’s dollars exist outside the United States

Most people assume that the global dollar system operates primarily inside the United States. Dollars are imagined as a national currency issued by the Federal Reserve, circulating through American banks and then flowing outward through trade, investment, and international finance.

This picture is incomplete.

A large portion of the world’s dollar-denominated financial activity occurs outside the United States entirely. The mechanism responsible is the Eurodollar system — a global offshore banking network that creates and circulates dollar credit beyond the direct control of U.S. monetary authorities.

Understanding this structure changes how the international monetary system must be interpreted.

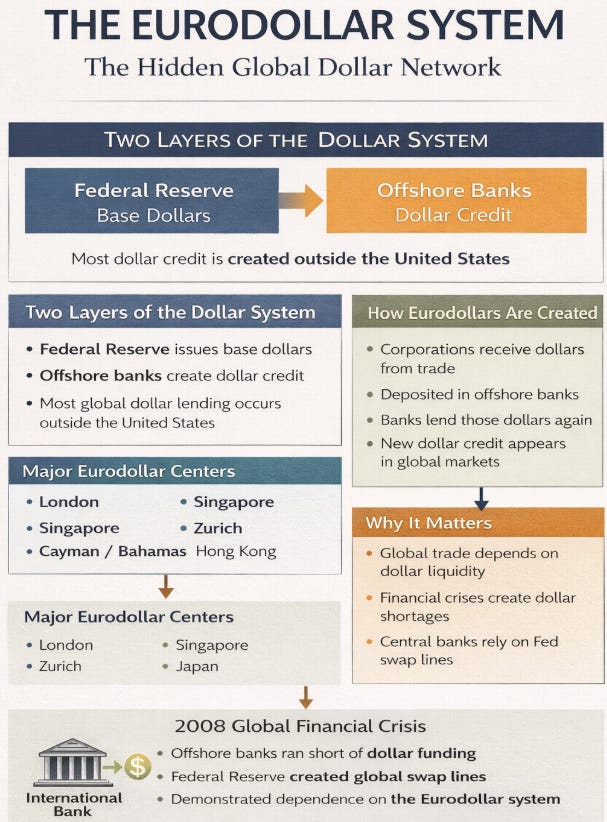

The Eurodollar system consists of U.S. dollar deposits held in banks outside the United States. These deposits are functionally identical to domestic dollars but exist beyond the direct regulatory framework of the U.S. banking system. When a bank in London, Singapore, Zurich, or Hong Kong holds dollar deposits and lends those dollars onward, it is operating within the Eurodollar network.

Over time this offshore market grew to extraordinary scale. Today the majority of global dollar credit creation occurs through balance sheets located outside the United States.

The origins of this system lie in the geopolitical and financial environment of the postwar period. After the Second World War the U.S. dollar became the dominant reserve and settlement currency. Governments, corporations, and banks around the world accumulated large dollar balances as international trade expanded.

Many of these deposits were held outside the United States, particularly in European financial centers. Banks quickly discovered that these dollar deposits could support lending and credit creation just like domestic bank deposits.

A bank in London could accept dollar deposits from a corporation in Brazil, lend those dollars to a company in Japan, and settle the transaction through correspondent banking networks. The credit was denominated in dollars but created entirely outside the United States.

This offshore dollar market expanded rapidly during the 1950s and 1960s. International banks realized that dollar funding could support a global credit system operating beyond domestic American regulation.

Several structural factors encouraged this growth.

Banks operating in the Eurodollar market were not subject to the same reserve requirements, interest controls, and regulatory constraints that existed inside the United States during the postwar period. This allowed offshore institutions to offer more competitive deposit rates and lending conditions.

Capital naturally migrated toward the system with fewer constraints.

Over time the Eurodollar network evolved from a peripheral financial mechanism into the central infrastructure of global dollar liquidity. International trade finance, corporate borrowing, sovereign debt issuance, derivatives markets, and interbank lending increasingly relied on offshore dollar funding.

Multinational banks built vast balance sheets denominated in dollars but located outside the United States.

The consequence is a monetary architecture that is widely misunderstood.

The Federal Reserve issues the base currency of the system. But it does not directly control the global creation of dollar credit.

That distinction is critical.

As examined in The Federal Reserve Is Different — and That Difference Is the Error, the Federal Reserve already occupies an unusual institutional position within the American constitutional structure. It functions as a central bank with substantial independence from ordinary political control. The Eurodollar system adds another layer of distance between monetary authority and the global dollar supply.

Large volumes of dollar credit are therefore created not by the Federal Reserve but by private international banks operating offshore.

In practice, the global dollar system consists of two interacting layers.

The first layer is the domestic monetary base issued by the Federal Reserve.

The second layer is the offshore credit network that multiplies and distributes dollar liquidity through international banking activity.

This second layer is the Eurodollar system.

From a structural perspective this produces an inversion within the monetary architecture. The institution commonly understood to control the currency — the Federal Reserve — manages the foundation of the system but not the majority of its expansion. The expansion occurs through private banking networks operating outside the jurisdiction in which the currency originates. Authority therefore appears centralized while operational power is distributed across international balance sheets. This separation between formal authority and functional control is a recurring pattern within modern institutional systems.

During periods of financial expansion the network can generate large volumes of dollar credit as banks lend aggressively against deposits and collateral. During periods of stress the same system can contract rapidly as institutions withdraw liquidity and reduce interbank exposure.

Because much of this activity occurs outside U.S. regulatory boundaries, the Eurodollar system introduces structural complexity into global financial stability.

Financial crises often reveal the extent of this hidden architecture.

The global financial crisis of 2008 demonstrated how deeply integrated offshore dollar markets had become with the domestic financial system. European banks had accumulated enormous dollar liabilities through Eurodollar funding markets while holding dollar-denominated assets.

When funding markets froze, these institutions faced severe shortages of dollar liquidity.

The response was not a purely domestic American intervention. The Federal Reserve created emergency dollar swap lines with foreign central banks, allowing them to supply dollars to their domestic banking systems. The objective was to prevent a collapse of the offshore dollar funding network.

As examined in The Global Financial Crisis and the Architecture of System Protection, the crisis response revealed how the financial system protects its core institutions when systemic stability is threatened. Dollar liquidity was extended globally in order to stabilize large international banks whose balance sheets depended heavily on Eurodollar funding.

The episode demonstrated that the stability of the global dollar system depends not only on domestic monetary policy but on the functioning of the offshore credit network itself.

This dynamic helps explain a recurring phenomenon in financial markets.

Liquidity conditions can tighten globally even when domestic U.S. monetary policy appears relatively stable. The reason is that the supply of dollar credit is determined not only by Federal Reserve actions but also by the behavior of international banks operating within the Eurodollar system.

Dollar liquidity is therefore a global balance-sheet phenomenon.

This observation also connects directly to the pattern described in The Liquidity Illusion, where financial markets can appear stable or rising even while underlying systemic fragility increases. When offshore credit expansion masks structural weaknesses, liquidity conditions may deteriorate rapidly once the Eurodollar system begins to contract.

Understanding this architecture clarifies why the dollar continues to dominate global finance.

The United States issues the currency. But the global financial system multiplies it.

The Eurodollar network functions as a transnational credit infrastructure linking banks, corporations, governments, and financial institutions across multiple jurisdictions. Through deposits, loans, derivatives, and securities markets, dollars circulate through a worldwide network that operates far beyond the borders of the country that issues them.

In this sense the Eurodollar system is not an anomaly.

It is the operational mechanism that allows the dollar to function as the world’s primary financial language.

Most of the world’s dollars do not reside in the United States.

They exist within a global banking network that continuously creates, distributes, and reallocates dollar credit across the international financial system.